Global Wood Charcoal Market Trends 2026: Strategic Analysis and Price Forecast

▶ Learn more about our Vinachaki charcoal: Video

Understanding the wood charcoal market trends 2026 requires analyzing macroeconomic volatility. Shifts in international trade policies, environmental technical barriers, and the relocation of manufacturing hubs are aggressively redrawing the global supply map. Consequently, these geopolitical shifts are the foundational drivers defining the wood charcoal market trends 2026.

Moving into the 2026-2027 operational cycle, this market transcends its legacy as a primitive raw material supply chain. It has evolved into a highly complex, multi-billion-dollar commercial ecosystem. Today, international trade flows are dictated absolutely by legal frameworks such as the European Union Deforestation Regulation, rigorous ESG standards, and the intense volatility of global green logistics.

This comprehensive report provides procurement directors, industrial buyers, and global distributors with a precise analytical roadmap. We will dissect the macroeconomic drivers, evaluate shifting segment demands, and deliver a definitive global wood charcoal price forecast to guide your strategic sourcing decisions.

Table of Contents

- 1. Macro Dynamics and Global Market Scale

- 2. Culinary Segment Preferences and Technical Specifications

- 3. Geopolitics, Trade, and Global Supply Axes

- 4. The EUDR Mandate and the “Clean Charcoal” Era

- 5. Pyrolysis Engineering and Retort Technology Evolution

- 6. The Rise of Biochar and Activated Carbon

- 7. 2026 Ocean Freight Logistics and Green Supply Chains

- 8. Detailed Global Wood Charcoal Price Forecast 2026-2027

- 9. Macroeconomic Risks and Market Challenges

- 10. Strategic Recommendations and Vinachaki Leadership

1. Macro Dynamics and Global Market Scale

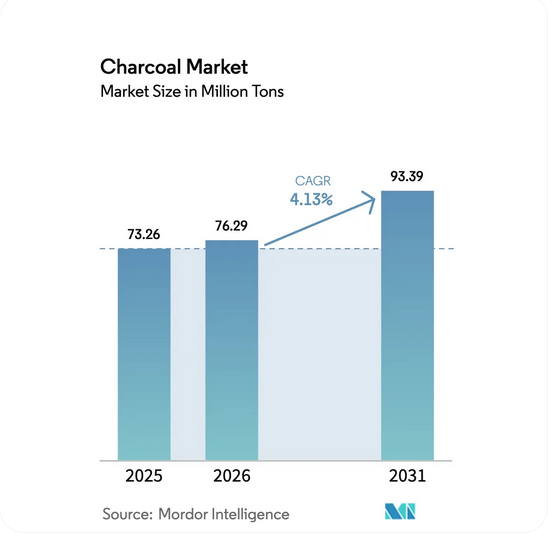

Evaluating the wood charcoal market trends 2026 requires a precise understanding of the underlying financial and volumetric momentum. The global charcoal market recorded a baseline valuation of $21.63 billion in 2024. Financial models project a steady expansion to $22.17 billion by 2025, charting a trajectory toward $27.01 billion by 2033. This represents a highly stable Compound Annual Growth Rate (CAGR) of 2.5%.

Global wood charcoal market trends 2026 and trade routes

More aggressive econometric models forecast the market scaling to $29.5 billion by 2034 with a 2.7% CAGR, reflecting explosive demand across both civil and heavy industrial segments. Volumetrically, the global economy consumed between 55 and 59 million tons of charcoal in 2024. Predictive analytics indicate this volume will surge to 76.29 million tons by 2026, eventually escalating to 93.39 million tons by 2031. This translates to a volumetric CAGR of 4.13% throughout the 2026-2031 forecast period.

This exponential growth stems from a multidimensional market shift rather than mere population increases. Key growth catalysts include the premiumization of outdoor barbecue culture in high-income demographics, the massive integration of activated carbon in municipal water treatment and pharmaceuticals, and the institutional adoption of biochar as a primary carbon sequestration tool.

Geographically, the Asia-Pacific region maintains absolute market dominance, commanding between 52% and 55.23% of total global volumes. North America registers as the fastest-accelerating region with a 2.6% CAGR, heavily driven by luxury grilling trends and the aggressive post-pandemic recovery of the foodservice sector. Application data reveals barbecue leading with a 45% market share, followed by industrial applications at 30%, and domestic heating securing the remaining 25%.

| Chỉ số thị trường | 2024 | 2025 (E) | 2026 (F) | 2031 (F) |

| Market Value (USD Billion) | 21,63 – 25,2 | 22,17 – 22,6 | 23,20 – 24,00 | 27,01 – 29,5 |

| Consumption Volume (Million Tons) | 55,0 – 59,0 | 73,26 | 76,29 | 93,39 |

| Value CAGR (%) | – | 2,5% | 2,5% – 2,7% | 2,5% – 2,7% |

| Volume CAGR (%) | – | – | 4,13% | 4,13% |

Key Growth Indicators of the Global Charcoal Market (2024-2031)

2. Culinary Segment Preferences and Technical Specifications

A core component of the wood charcoal market trends 2026 involves extreme fragmentation in professional culinary fuel selection. Every business model—from luxury Fine Dining to mass-market buffet chains and outdoor recreation—enforces distinct procurement criteria based strictly on thermal efficiency, smoke structure, and unit economics.

Fine Dining and Yakiniku: The Binchotan Imperative

Within the highest echelon of gastronomy, specifically Japanese Yakiniku and elite steakhouses, Binchotan (White Charcoal) retains an irreplaceable monopoly. Manufacturers engineer Binchotan through an intensely complex carbonization process exceeding 1000°C. Rapid cooling utilizing an ash and sand mixture creates an extraordinarily dense, metallic carbon structure.

The preference for Binchotan relies on its absolute purity. It burns completely smokeless, completely odorless, and entirely spark-free. In luxury dining environments, eliminating fuel-based impurities is an operational imperative. Binchotan emits powerful infrared heat, cooking proteins thoroughly from the core while preserving natural moisture and flavor profiles. Delivering an uninterrupted burn time of 4 to 5 hours, it allows restaurants to optimize service workflows effortlessly.

Buffet Chains and Mass BBQ: Sawdust Briquette Efficiency

Mass-market buffet chains and large-scale BBQ franchises operate on rigorous cost-optimization and quality uniformity principles. Consequently, Sawdust Briquettes dominate this segment. Factories compress natural wood sawdust under extreme high pressure into uniform hexagonal or square extrusions prior to carbonization.

Sawdust briquettes represent the ultimate intersection of thermal performance and economic viability. Featuring a fixed carbon content exceeding 80% and negligible ash residue (typically under 2-4%), these briquettes provide a highly stable burn lasting 3.5 to 4.5 hours. The strict dimensional uniformity allows floor managers to standardize fuel allocation per table, maintaining absolute control over operational overhead. Furthermore, the smokeless nature of high-grade sawdust charcoal drastically reduces the load on expensive HVAC and ventilation systems in enclosed dining spaces.

Outdoor BBQ and Domestic Retail: The Hardwood Lump Transition

In mature consumer markets across the US and Europe, behavioral data indicates a massive migration away from chemically treated briquettes toward Natural Hardwood Lump Charcoal. Modern consumers prioritize health, sustainability, and authentic culinary experiences. Premium hardwood lump crafted from oak, hickory, or mesquite satisfies these exact criteria.

Lump charcoal commands consumer loyalty due to its rapid ignition capabilities and extreme peak temperatures, making it the superior choice for searing heavy proteins. While burn times are shorter than compressed briquettes, the distinct, delicate smoke profile imparted by natural forest timber remains the deciding factor for BBQ enthusiasts. Retail market analysis shows over 75% of US households own a grill, with a rapidly increasing majority exclusively demanding “100% natural” or “additive-free” fuels.

| Culinary Segment | Preferred Charcoal | Core Technical Characteristics | 2026 Price Forecast (USD/Ton) |

| Fine Dining / Yakiniku | Binchotan (White Charcoal) | Smokeless, infrared heat, >5 hrs burn time | $1,350 – $1,650 |

| Buffet / BBQ Chains | Sawdust Briquettes | Uniform shape, low ash, clean burning | $700 – $950 |

| Outdoor BBQ (US/EU) | Hardwood Lump Charcoal | Quick ignition, natural smoke flavor | $700 – $850 |

| Domestic BBQ (Economy) | Black Charcoal (Acacia/Eucalyptus) | Economical, highly available, easy ignition | $380 – $500 |

| Shisha / Hookah | Coconut Shell Charcoal | High heat, odorless, white ash | $800 – $1,400 |

Charcoal Preference Matrix by Culinary Segment

3. Geopolitics, Trade, and Global Supply Axes

Understanding the wood charcoal market trends 2026 requires analyzing macroeconomic volatility. Shifts in international trade policies, environmental technical barriers, and the relocation of manufacturing hubs are aggressively redrawing the global supply map.

The Asian Production Axis and Southeast Asian Ascent

The Asia-Pacific region operates as both the largest consumer base and the central manufacturing engine of the global charcoal industry. Indonesia, Vietnam, and the Philippines continue to solidify their positions as apex exporters. These nations leverage massive biomass reserves derived from agricultural by-products (coconut shells) and sustainable timber plantations (acacia, eucalyptus, and rubberwood).

Indonesia currently commands the global export volume lead, specifically dominating the coconut shell and shisha briquette segments, dispatching over 41,800 tons monthly. Conversely, Vietnam executes a distinct strategy. Exporting approximately 6,366 tons monthly, Vietnam successfully positions itself as the premium manufacturing hub. Vietnamese facilities offer the world’s most sophisticated and diverse product portfolio, ranging from elite Binchotan to heavy-duty sawdust extrusions.

South America and Africa: Strategic Commodity Reserves

Brazil reigns as the world’s largest exporter of wood products (HS Code 44), generating $13.3 billion in 2025 export value to capture 66% of the global market share. Massive, industrialized eucalyptus plantations sustain the Brazilian charcoal sector, which primarily services domestic metallurgy and bulk US export channels. Paraguay operates as a critical South American specialist, supplying high-density Quebracho hardwood charcoal to exacting European buyers.

In Africa, nations like Nigeria and Ethiopia function as vital sources for commodity-grade heating and cooking charcoal. However, these supply chains face mounting regulatory pressure regarding forest management. The Nigerian government recently enacted strict export guidelines mandating transparent reforestation initiatives and sustainable forestry commitments to secure export licenses. This signals a permanent global tightening of raw material accessibility.

4. The EUDR Mandate and the “Clean Charcoal” Era

Without question, the most disruptive macroeconomic variable shaping the wood charcoal market trends 2026 is the European Union Deforestation Regulation (EUDR). Although the EU delayed full enforcement to December 30, 2026, for large corporations and June 30, 2027, for SMEs, its systemic impact already dictates current procurement contracts.

The EUDR creates an impenetrable legal barrier. It mandates all importers to provide absolute, scientific proof that their imported products possess zero links to deforestation or forest degradation occurring after December 31, 2020. This requires deploying sophisticated traceability systems reliant on exact geolocation data.

For major exporting nations like Vietnam and Brazil, compliance necessitates massive capital investment in land data digitization and forestry management protocols. Manufacturers capable of supplying FSC-certified charcoal or verifiable EUDR-compliant documentation command an immediate, unassailable competitive advantage. In the European market, these compliant suppliers currently extract a 10% to 30% price premium. This regulatory environment accelerates the eradication of informal, artisanal producers, forcing the market toward extreme professionalization.

5. Pyrolysis Engineering and Retort Technology Evolution

The charcoal manufacturing sector is executing a massive technological pivot, which stands as a defining pillar of the wood charcoal market trends 2026. Transitioning away from archaic manual processes, the industry is widely adopting advanced pyrolysis systems. This engineering evolution directly addresses tightening global emission standards and modern occupational health requirements, perfectly aligning with the overarching wood charcoal market trends 2026.

Traditional Kilns vs. Closed Retort Systems

Legacy manufacturing methods utilizing open earth pits or basic brick kilns generate catastrophic environmental pollution. These systems release massive volumes of untreated methane (CH4) and carbon monoxide (CO) directly into the atmosphere. Furthermore, their economic efficiency is abysmal, typically yielding a wood-to-charcoal conversion rate below 20%.

The deployment of Retort Kiln technology fundamentally alters production economics. Retort systems utilize a closed-loop engineering architecture. The highly combustible gases generated during the pyrolysis phase are captured rather than vented. The system redirects these gases back into the primary combustion chamber to fuel the continuous carbonization process.

This thermodynamic efficiency increases biomass conversion yields to 30%-45% while simultaneously eliminating up to 75% of toxic emissions. Elite systems, such as CharcoTec architectures, capture residual thermal energy to pre-dry fresh timber, achieving maximum energy optimization. In highly regulated markets like Germany and Japan, charcoal produced via retort technology serves as the baseline requirement for premium product classifications.

| Comparison Criteria | Traditional Earth/Brick Kiln | Flame-Curtain Kiln (Kon-Tiki) | Modern Retort Kiln |

| Conversion Efficiency (%) | 15% – 20% | 20% – 25% | 30% – 45% |

| Carbonization Time | 5 – 10 days | 3 – 5 hours | 24 – 48 hours |

| Fixed Carbon Content | Low, inconsistent | Medium (~75%) | High (>82%) |

| Emissions (CO, CH4) | Very high | Low (75% reduction) | Very low (closed-loop system) |

| Investment Cost | Very low | Low – Medium | High (>$500,000) |

Efficiency and Environmental Impact Comparison of Pyrolysis Kilns

6. The Rise of Biochar and Activated Carbon

Analyzing the wood charcoal market trends 2026 requires acknowledging the blurring boundaries between culinary fuels and advanced environmental tools. Biochar created via the pyrolysis of agricultural waste has rapidly matured into a primary revenue driver through the international carbon credit market.

Biochar projects operating in Australia, Brazil, and the US generate lucrative carbon removal credits based on the material’s verified capacity to sequester carbon securely in soil for centuries. Simultaneously, heavy industries including steel and cement manufacturing in China and India are aggressively integrating biochar to partially replace metallurgical coke in blast furnaces. This strategy aims to drastically reduce industrial carbon footprints by 2028. This cross-sector demand triggers intense competition for raw timber, inadvertently establishing a high price floor for standard hardwood charcoal.

Activated Carbon: Technical Water Treatment and Pharma

Activated charcoal represents the highest-value derivative in the carbon sector. In Europe, where over 80% of municipal freshwater originates from vulnerable groundwater and river sources, authorities are massively scaling activated carbon filtration to absorb toxic organic compounds.

In the United States, the Environmental Protection Agency recently enacted strict limitations on PFAS in drinking water. Municipalities are urgently overhauling filtration infrastructure with premium activated carbon to ensure compliance. Analysts project the technical water filtration segment will achieve a 12% volume growth rate, easily outpacing standard fuel markets. Additionally, the pharmaceutical and cosmetics industries continue demanding ultra-pure activated charcoal for detox formulations and deep-cleansing products, creating a niche market valued at thousands of dollars per ton.

7. 2026 Ocean Freight Logistics and Green Supply Chains

Logistics architecture dictates between 20% and 40% of the final landed cost for international charcoal shipments, making it a crucial component when calculating the global wood charcoal price forecast. Entering 2026, the global maritime shipping market transitions into a new normal, stabilizing after the extreme volatility of the pandemic era and directly impacting the wood charcoal market trends 2026.

Capacity Oversupply and Freight Rate Contraction

The 2026 shipping market faces a massive influx of new container vessel capacity, the result of aggressive fleet ordering between 2021 and 2023. Global fleet capacity expanded by roughly 28% over five years, generating severe oversupply across major East-West arterial routes.

Consequently, container freight rates from Asia to North America and Europe will remain significantly below peak crisis levels. Predictive models place the Shanghai to Los Angeles route between $1,200 and $1,800 per FEU, an 85% contraction from the $12,000 apex recorded in 2022. Routes to Rotterdam exhibit identical deflationary trends. This environment presents a critical strategic window for exporters in Vietnam and Indonesia to optimize profit margins or deliver more aggressive pricing to Western distributors.

Green Surcharges and Technical Port Barriers

While base freight rates decline, environmental compliance fees are accelerating. The expansion of the EU Emissions Trading System to include the maritime sector forces shipping lines to purchase carbon allowances for vessel emissions. Carriers pass these costs to shippers as Green Surcharges, adding $150 to $400 per container.

Furthermore, authorities classify charcoal as a sensitive, potentially hazardous cargo due to spontaneous combustion risks. Customs officials at major EU and Japanese ports enforce increasingly stringent inspections regarding container moisture levels and particulate cleanliness. Non-compliance immediately triggers severe demurrage penalties and supplementary inspection fees, easily inflating logistics costs by $15 to $30 per ton.

8. Detailed Global Wood Charcoal Price Forecast 2026-2027

A definitive and accurate global wood charcoal price forecast for the 2026-2027 cycle indicates a moderate, highly sustainable upward price adjustment. Formidable cost-push factors including escalating labor wages, energy inputs, and regulatory compliance overhead establish an absolute floor against any significant price reductions. Procurement managers must utilize this global wood charcoal price forecast to navigate the complex wood charcoal market trends 2026 effectively

Wholesale and Export Price Dynamics

Global wholesale charcoal valuations will experience a 5% to 12% increase in 2026 compared to 2025 baselines. While 2025 commercial-grade charcoal traded between $280 and $450 per ton, the 2026 median shifts aggressively toward the $300 to $500 per ton spectrum. For professionally packaged, retail-ready inventory holding verified quality certifications, FOB export prices will confidently breach the $380 to $650 per ton threshold.

Three primary vectors drive this structural inflation. First, raw material costs are surging as forestry management tightens in regions like Nigeria, restricting access to cheap timber. Second, ESG compliance overhead specifically the continuous operational cost of running EUDR geolocation traceability software consumes 5% to 20% of SME revenue. Third, charcoal manufacturing remains a labor-intensive industry. Rising statutory minimum wages in critical production hubs like Vietnam and Indonesia directly inflate manual sorting and packaging expenses.

The Vietnam FOB Price Benchmark: 2026 Forecast Methodology and Data

Global importers consistently utilize Vietnam as the definitive price benchmark for Asian manufacturing due to the country’s unmatched product diversity and stringent quality control standards. To ensure absolute accuracy in our global wood charcoal price forecast, these baseline projections are synthesized from primary supply chain data, including direct procurement metrics from leading export consortia such as the Vietnam Charcoal Team; Thạnh Đỗ Supply and Vinachaki.

Before examining the specific asset classes, industry leaders must understand the structural cost-push factors establishing this new price floor. The upward trajectory within the current wood charcoal market trends 2026 is driven by three inescapable macroeconomic realities:

-

Raw Material Deficits: Strict forestry governance globally (such as export tightening in Nigeria) and intense competition from high-value furniture and plywood sectors severely restrict access to cheap timber.

-

ESG and EUDR Compliance Overhead: Deploying continuous GPS geolocation software and maintaining rigorous traceability documentation is not a one-time setup. It is a continuous operational expense, consuming between 5% and 20% of SME revenue.

-

Labor Inflation: Charcoal production remains highly labor-intensive. Statutory minimum wage increases across major Southeast Asian hubs directly inflate manual sorting, cutting, and packaging expenses.

Consequently, the baseline FOB export prices from Vietnam project the following valuations for the 2026-2027 cycle:

-

Binchotan (White Charcoal): $1,350 – $1,650 per ton. Pricing reflects extreme manufacturing complexity (>1000°C carbonization) combined with surging Japanese/Korean Fine Dining demand for >82% fixed carbon and zero-smoke, 5-hour burn times.

-

Premium Sawdust Briquettes (VIP Grade): $700 – $950 per ton. Driven by massive BBQ buffet chain expansion requiring absolute physical uniformity, >80% fixed carbon, and low ash residue to optimize commercial HVAC systems.

-

Hardwood Lump (Longan/Khaya): $700 – $850 per ton. Backed by highly stable US/EU Steakhouse demand and premium retail sectors aggressively transitioning away from chemical briquettes.

-

Softwood/Coffee Charcoal: $650 – $750 per ton. Supported by consistent high demand from domestic retail channels and outdoor enthusiasts seeking rapid ignition and natural smoke profiles.

-

Commodity Acacia Charcoal: $380 – $500 per ton. Facing declining global demand and price stagnation due to environmental pressures, low fixed carbon (<65%), and rapid consumption rates.

Pricing ultimately diverges based on the destination market’s specific risk tolerance. Japan and South Korea, enforcing flawless clean-charcoal standards, readily absorb a 20% local premium for ultra-high-grade products (such as mangrove charcoal) compared to Middle Eastern buyers. Conversely, hyper-competitive retail dynamics in the US force major brands to absorb production cost increases internally. To defend profit margins amidst the evolving wood charcoal market trends 2026, these US manufacturers urgently innovate via “flavor-infused” or verified “organic sawdust” labeling.

9. Macroeconomic Risks and Market Challenges

Despite robust growth projections, the wood charcoal market trends 2026 carry significant operational risks capable of disrupting supply chain continuity.

Beyond EUDR implementation, aggressive PM2.5 (fine particulate matter) emission regulations threaten urban charcoal consumption. During severe smog events in New Delhi, municipal authorities implement emergency bans on commercial charcoal grills, forcing restaurants to temporarily adopt gas or electric alternatives. This strict regulatory approach may rapidly replicate across other heavily polluted Asian and European metropolises.

Financial volatility presents another distinct challenge. Charcoal transactions settle predominantly in US Dollars (USD). Persistent USD strength or sudden currency devaluations in exporting nations like Brazil or Indonesia can violently distort FOB pricing structures overnight. Furthermore, persistent inflation across the Eurozone threatens consumer purchasing power, potentially constricting discretionary spending on outdoor leisure and BBQ activities.

Finally, climate change directly destabilizes production output. Erratic, prolonged monsoon seasons across Southeast Asia critically disrupt timber drying phases and extend carbonization cycles. These weather anomalies trigger localized supply deficits, causing spot market prices to spike unpredictably. Such environmental disruptions are severe risk factors that can instantly invalidate any standard global wood charcoal price forecast and disrupt the overarching wood charcoal market trends 2026.

10. Strategic Recommendations

The wood charcoal market trends 2026 represent the convergence of three monumental forces: the premiumization of culinary demands, the absolute digitization of supply chains, and the industrialization of pyrolysis engineering. Charcoal has shed its identity as a primitive fuel to become a highly specialized, technically rigorous commodity. Navigating the wood charcoal market trends 2026 requires agility and precise data utilization.

Strategic Imperatives for Global Importers

Importers and international distributors must execute a multi-sourcing strategy. Over-reliance on a single geographic region or a single charcoal variant exposes businesses to fatal supply chain ruptures. Blending South American Hardwood Lump, Southeast Asian Sawdust Briquettes, and Coconut Shell ensures a highly resilient, agile product portfolio. Furthermore, importers must leverage the 2026 logistics window—utilizing current low freight rates to negotiate long-term shipping contracts and secure warehouse inventory before Green Surcharges escalate further.

Vinachaki: Engineering the Future of Global Carbon

The upcoming 2026-2027 cycle will ruthlessly filter the market. Only manufacturers prioritizing absolute sustainability, elite technical performance, and strict macroeconomic compliance will survive. This is the exact operational framework where Vinachaki establishes its global leadership.

Vinachaki does not merely participate in the market; we actively engineer its future. By synthesizing Vietnam’s vast, sustainable biomass reserves with cutting-edge, low-emission retort technology, Vinachaki guarantees an elite, 100% compliant global supply chain. We eliminate the legal and financial risks associated with EUDR compliance by providing absolute transparency and rigorous origin traceability.

Whether your market demands flawless Binchotan for Michelin-starred Yakiniku, ultra-dense sawdust briquettes for commercial franchises, or pure hardwood lump for premium retail, Vinachaki delivers uncompromising quality at stable, highly competitive FOB rates.

Secure your 2026 supply chain today. Partner with the visionary leader in sustainable carbon manufacturing. Contact the Vinachaki Global Export Team to request technical specifications, arrange compliance audits, and secure your long-term volume contracts.

-

📞 WhatsApp/Hotline: (+84) 868 601 809

-

📧 Email: info@vinachaki.com

-

🌐 Website: vinachaki.com

-

📍 Address: 13 Street No.17 Lakeview City Residence, Binh Trung Ward, Ho Chi Minh City, Vietnam